A Century?!

What Alphabet's new 100-year hot issue says about the fixed income market

The following views are my own and do not represent the views of TD Securities whatsoever.

On Feb 13th, Alphabet, the owners of Google, unleashed a behemoth of a bond issue in the market, specifically the UK market.

The bond is an ultra rare issue that matures on Feb 13, 2126 and pays a 6.125% coupon. This is something that hasn’t been seen since Motorola released their 100 year issue back in 1997, during the heights of the Dot Com Bubble.

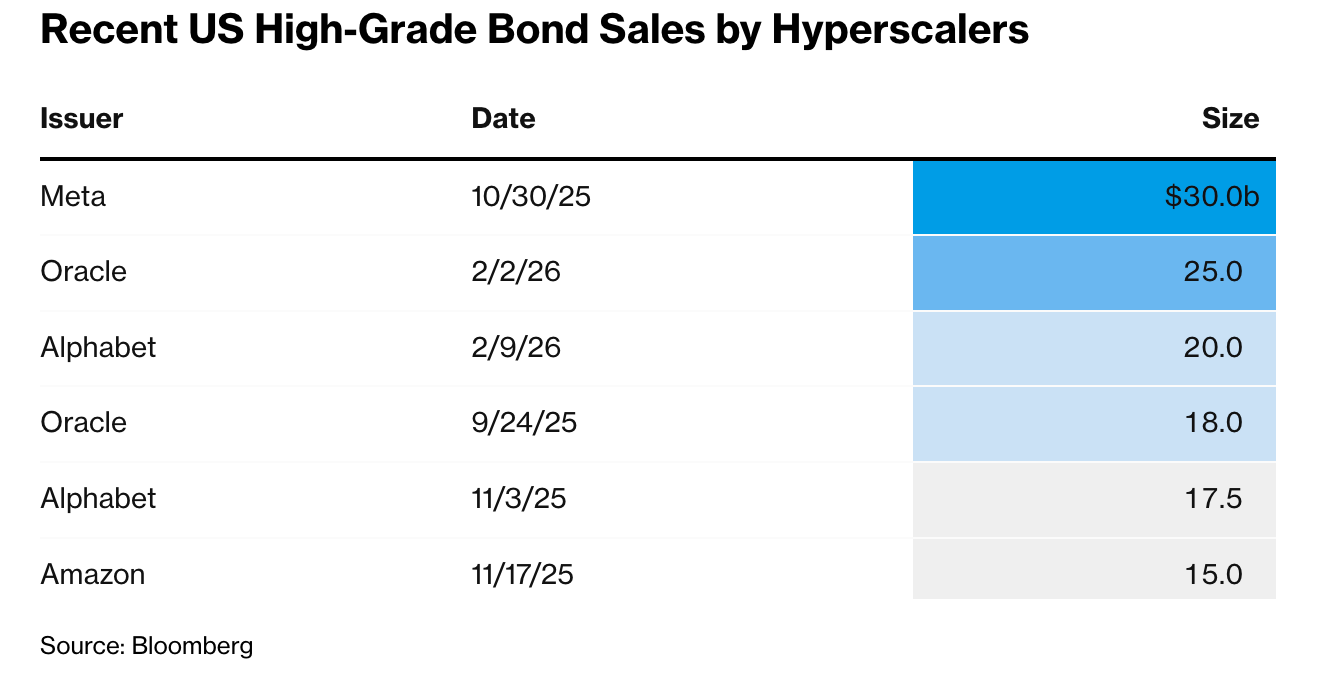

It came as an effort by Alphabet to raise funds for its AI ambitions. In that week, the company was able to raise $32 billion in less than 24 hours and came with $100 billion in orders for its US new issues.

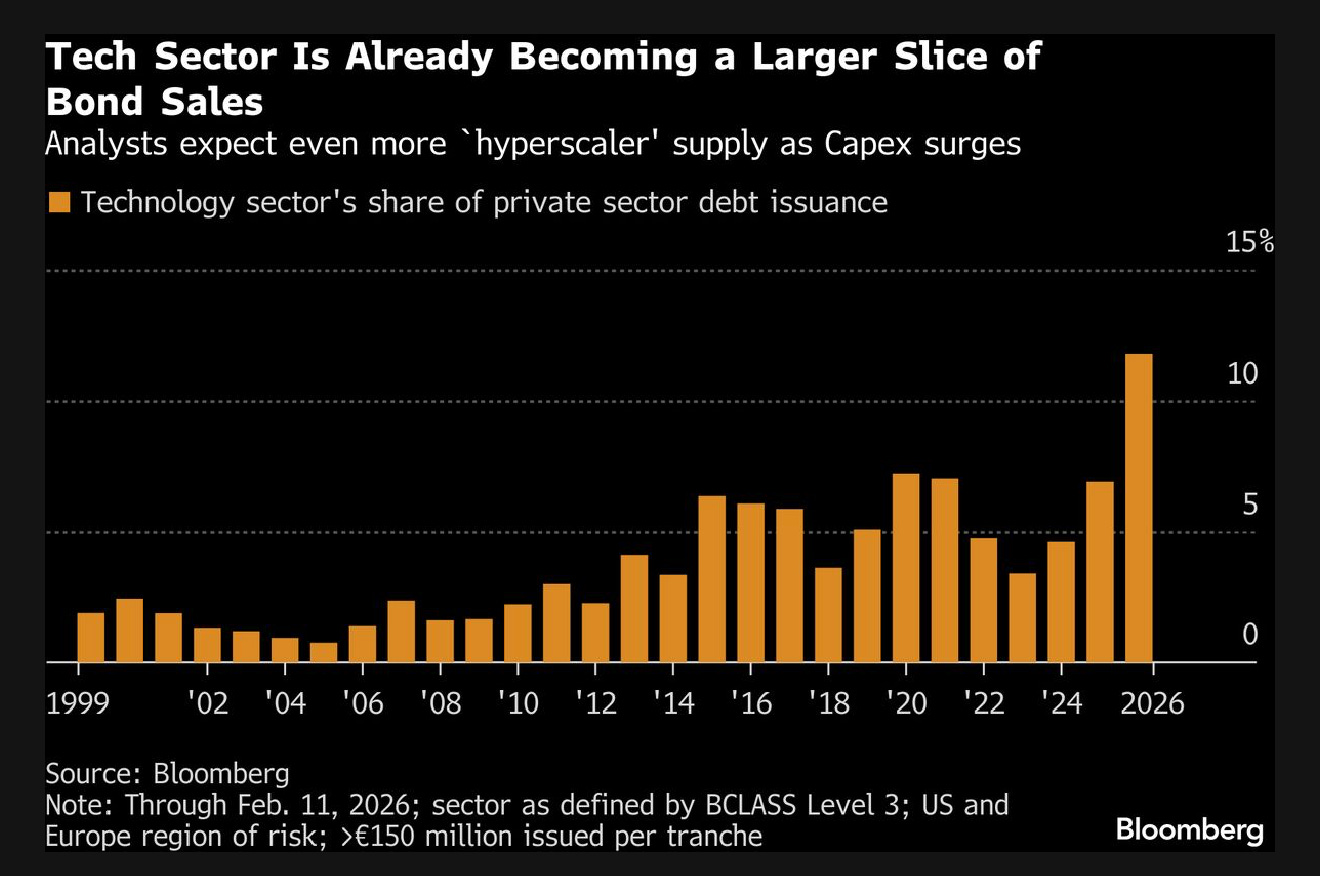

The portion of issues in the UK has made them one of the largest issuers in sterling IG debt, with its 100 year issue being 10 times oversubscribed.

This new package of corporate bonds is saying a lot about where the fixed income market is at right now.

Alphabet is not the only hyperscaler going through this trend. Oracle drew in $129 billion in demand for its $25 billion issue. Morgan Stanley expects borrowing by these cloud computing giants to reach $400 billion in 2026, up from $165 billion in 2025.

That’s not it. These hyperscalers are reaching across the yield curve, attracting a variety of investors from hedge funds to insurance firms and pensions. Alphabet has issued maturities between 3 years and 100 years.

They are also reaching across the globe, tapping in to the European bond market, from Switzerland to London, looking for new untapped sources.

I mentioned in a previous article that the bond market is like wine tasting. If you stick with me and this metaphor, we can see that these giants are giving investors the whole winery, with every flavour for all to try.

So what does this mean for the high-grade bond market?

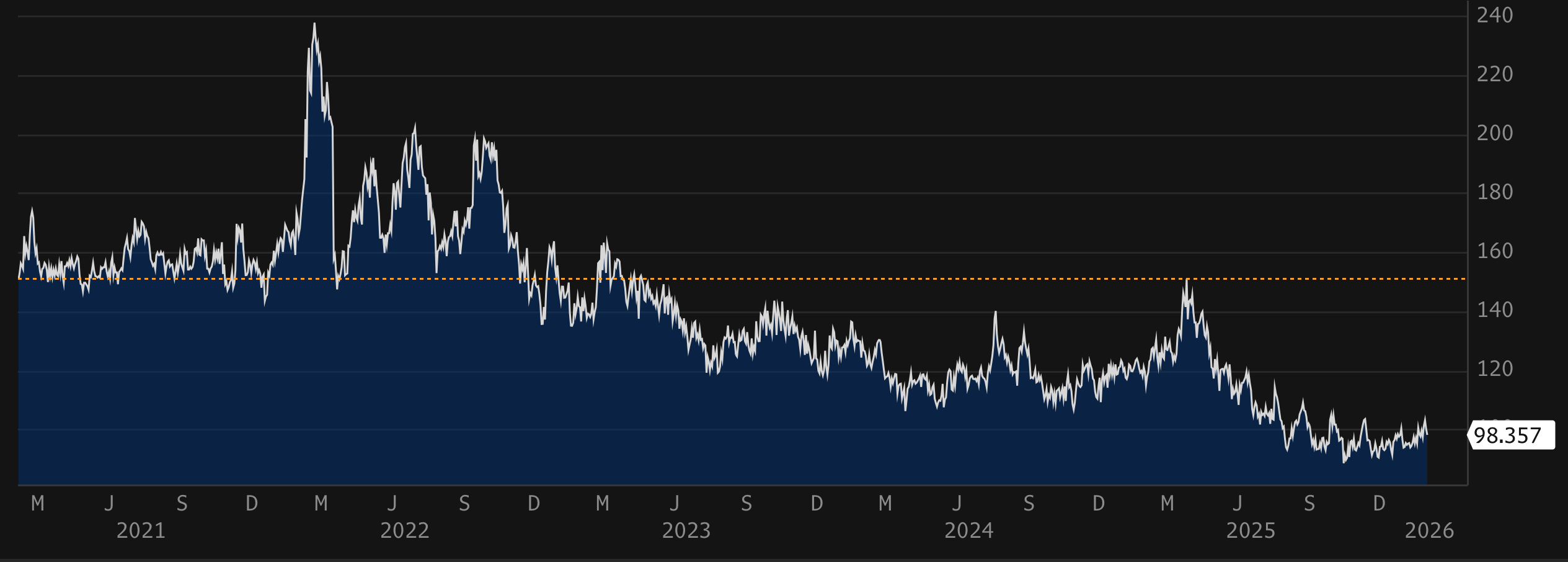

Bond Rush

JPM EMBI Global IG Sovereign Spread

Lower spreads indicate that demand for IG corporates is at unprecedented levels. If that wasn’t true, Alphabet’s century long issuance would not be 10x oversubscribed.

Investors of varying appetitees are therefore lining up for an incoming large supply of bonds at very low spreads.

There are two key questions that we need to be on the lookout for:

Can this supply be sustainable? Can hyperscalers keep issuing more and more? This is contingent on their capacity to borrow and the success of their AI operations in the next few years.

Can this demand be sustainable? Will investors keep on accepting issues at such low prices? At this point, it seems that the appetite for new and shiny AI spending is overpowering the desire for better yields.

Looking at supply, we seem to be expecting $400 billion in new issuances from these tech giants. This would only be possible if the companies are confident in their borrowing capabilities, as well as their ability to gain a return on their investments.

This is also dependent on the success of the AI train, which seems to be going full steam ahead with companies pouring cash into projects. Before it raised its new bond issues, Alphabet announced that it expects its CAPEX to reach as much as $185 billion this year, which is double what it spend last year.

On the demand side, it depends on whether investors can take lower spreads. The hyperscalers are testing the markets and investors are giving them a standing ovation from across the curve. Soon enough, if demands keeps up like this, a corporate IG bond from an issuer investing in new technology that has an uncertain future will have the same spread implied risk as a sovereign bond, which doesn’t really make sense.

What I fear is that spreads for this sector would become weak measures of investor sentiment on industry risk, since the hype is overpowering risk aversion.

Not saying that you should be risk averse when looking at tech issues, but looking at the trend of IG credit, we can see that investors are deciding to forgo a portion of yield to subscribe to AI bond issues - something that needs to be monitored.

Answering the two questions requires monitoring this situation for the rest of the year and seeing how investors receive new issues.

The profitability and potential of the AI train needs to be analyzed, as well as investor appetite for lower spreads.

Hope this cleared the fog this morning.