Bond Vigilantes

The Market is Making Demands and They Need an Answer

The following views are my own and do not represent the views of TD Securities whatsoever.

The word ‘vigilante’ is broadly defined as someone who is a “self-appointed doer of justice” by Merriam Webster.

But in the bond universe, things are different.

Justice in this world means proper compensation for risk, and interestingly, the vigilantes are not self-appointed.

Nevertheless, during Clinton’s time from 1993 to 1994, “bond vigilantes” seemed to be the fitting term.

During that time, US 10-year yields rose from just below 5.5% to about 7.8% in response to budget deficits under Clinton, who had to then legislate measures to control the deficit, which then brought yields back to pre-1994 levels by the end of 1995.

After these events unfolded, James Carville said that he “used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.”

Bond vigilantism is a phenomenon where investors demand higher compensation in response to excessive spending or over-expansionary monetary policy.

The reason we bring them up today is to assess whether they have returned.

Laying the Base

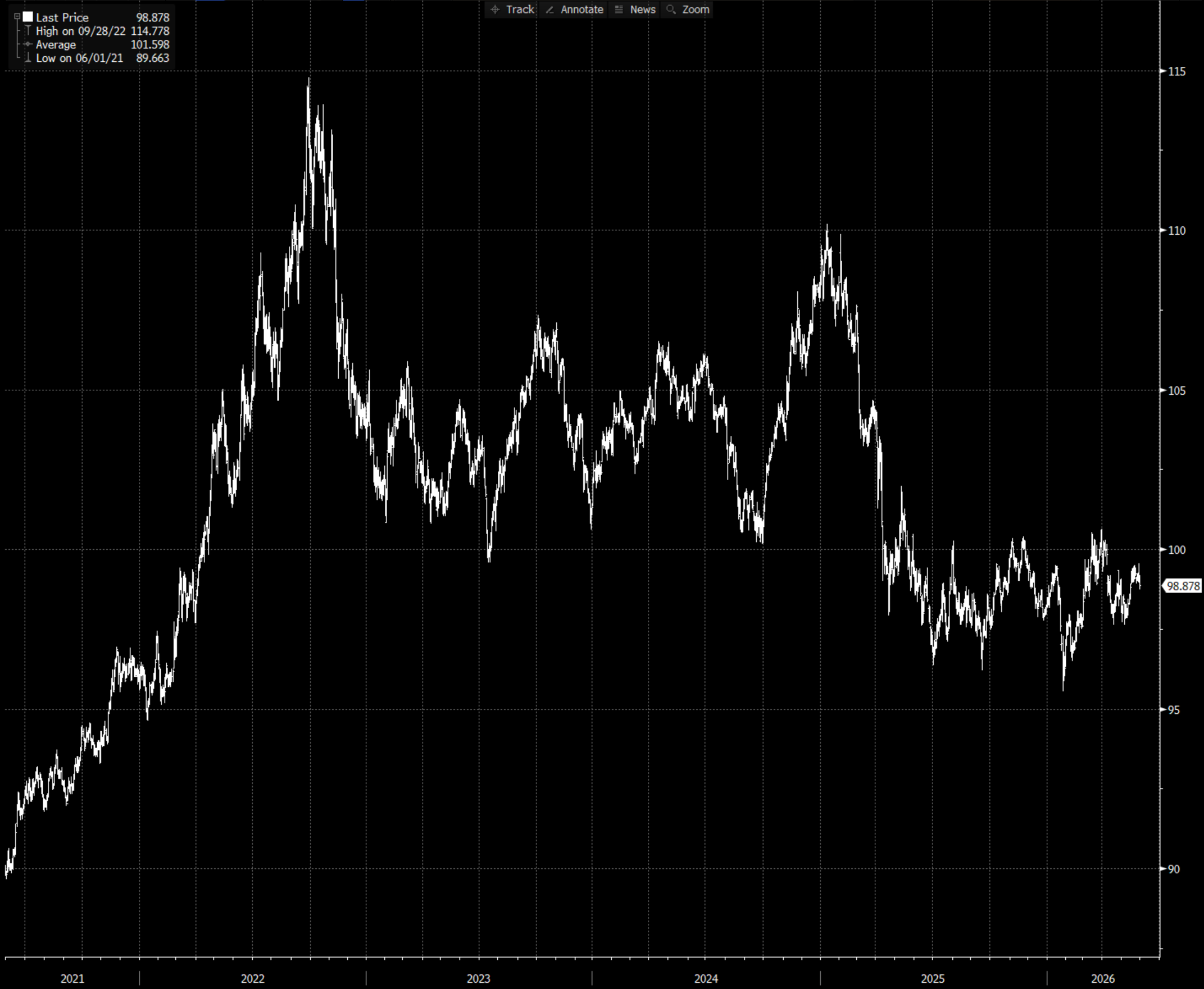

The US 10Y this time around has increased from 3.9375% to around 4.4492% at the time of writing. A headline that floated around last week was how US 30Y yields reached levels above 5% for the first time since around 2007.

There are a few themes driving this move:

The Debasement Trade: frequently discussed before. The traditional move away from US sovereign bonds and currencies as ‘safe havens’ should naturally add some risk premium on yields.

Fed governance: Now that Warsh is sworn in as Fed chair, there is some concern over whether policy decisions will remain independent.

Geopolitical tensions: although there are hopes for a ceasefire deal, the Middle East will not be the same as before. Someone will have to pay for that risk.

These three themes are drawing bond vigilantes out.

And it’s working.

Federal Funds futures are pricing in a full 25 bps hike by Sept. 2027, in contrast to Bowman’s statement, where she supported maintaining language that suggested additional rate cuts are possible.

We will delve into each theme and assess validity.

Still a Safe Haven?

The debasement trade is a recent market phenomenon where investors around the globe are choosing Gold and Crypto rather than US treasuries and the USD as safe havens in times of tension. This theme is backed by the rise of oil prices through the last few years and the stagnation of the US dollar since the beginning of 2025.

Although there was a sell-off in Gold where the metal shed 15% of its value in a matter of a few months, Gold prices still sit at about a 1.5x premium to prices in 2023.

Although JP Morgan reports that the debasement trade is cooling due to large Bitcoin ETF outflows amid hopes for an end to the conflict, the theme is nevertheless concerning.

In March 2026, The US Treasury Department reported that foreign official institutions were net sellers of $14.9 billion in long-term US securities, even as private foreign investors were net buyers of $111.4 billion.

US Treasury wise, the debasement trade reflects a shift in the composition of holders rather than a shrinking of demand.

In the dollar space, the erosion is much clearer.

The dollar’s share of global foreign exchange reserves has declined from over 70% to 56.8% in Q4 of 2025.

This debasement is not founded on nothing:

The US public debt-to-GDP ratio stands at around 122%, with a federal fiscal deficit that stands at 5.8% of GDP projected for 2026.

Interest expenses now consume ~51% of tax revenue and account for over 80% of the fiscal deficit.

These are not so pleasant signals.

In summary, US Treasury holdings are moving from foreign official institutions, which would hold these long-term securities on reserve, to private foreign investors, who are more price sensitive.

This means that those same price sensitive investors are going to demand risk premiums for US fiscal inefficiency, giving rise to bond vigilantism psychology within the investor population.

Political Bombardment of the Fed

Central Bank independence is crucial for our economic well-being.

It has been proven that central bank independence around the world is linked to lower inflation. This is because a less independent central bank might prioritize short-term employment and growth over the risk of future inflation.

Periods where credibility of central banks have been questioned have historically coincided with times of increased interest rate volatility and term premia. This leads to an increase in risk premia across all assets, prompting investors to partially de-risk.

This is why when investors talk of central bank credibility, it is taken very seriously.

President Trump has continuously criticized former Fed Chair Jerome Powell over his interest rate policy. Trump has a bias to prioritizing short-term growth over long-term inflation. This has raised concerns over the future of the Fed.

European Central Bank President Christine Lagarde stated that the Fed’s independence is “not a settled matter”.

This concern obviously needs to be accounted for in the markets.

In the case of the Fed, we would need more time to assess their stance; are they going to kow-tow to Trump and keep their cutting bias or are they going to uphold the Fed’s credibility?

Yardeni Research urged the Fed to drop its easing bias or investors will conclude that the central bank is no longer independent, motivating bond vigilantes to rise.

The next June meeting will be crucial in determining whether credibility will be an ongoing concern or not. But for the time being, this uncertainty will definitely raise premia across the curve.

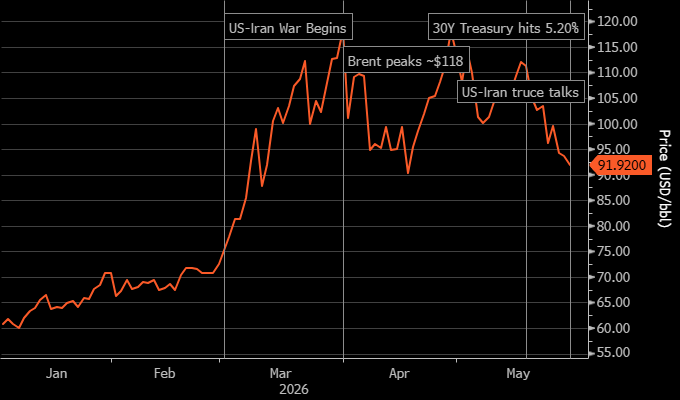

It’s All About Oil

As of when this article was written, Trump is still deliberating his final decision on a ceasefire. This has pushed Brent lower and yields have briefly contracted.

However, it is not all sunshine and rainbows here.

The halt of traffic through the Strait of Hormuz has created a supply disruption, pushing energy prices up. Additionally, fertilizer prices have been affected as well, as a large portion of fertilizer passes through the narrow strait.

Even after the conflict ends, it is expected that production will remain below pre-war levels throughout 2026. Water Tower Research states that this is because of:

Pressure loss in wells that have been shut in.

Necessary repairs to damaged infrastructure.

Worker displacement from conflict zones.

We would even contend that oil prices will never reach pre-war levels.

Think about it: the difficulty in kickstarting production again, combined with Iran’s intention to place tolls on passing carriers, will add a premium on energy prices.

This doesn’t even account the sense of security in the strait, which may never be fully restored. The Gulf will always be at a tipping point from now on. Bond investors will demand return for a geopolitically unpredictable government.

With no resolution to the conflict, inflation risk will still be topical.

A State of Mind

To clarify, bond vigilantes are not self-appointed, as the definition of ‘vigilante’ would suggest.

Instead, the circumstances appoint them.

Bond vigilantes are simply investors speaking to where they think risk premia should sit.

For June, the Fed meeting will be crucial to watch. This meeting will give direction to whether Fed independence can be truly called into question.

However, premiums for geopolitical risk and lax fiscal policies will remain for a while.

For worries to subside, we have to see the following signals:

Action towards a more responsible fiscal policy.

A return to a moderate and predictable US foreign policy.

Until we reach that point, bond vigilantism will remain a topic of discussion in macro circles.

Hope this cleared the fog for you today.

Banging article